Small Saving Schemes Interest Rate July–Sept 2025 Update

Understanding the Small saving schemes interest rate can be the difference between passive saving and smart wealth-building. For U.S.-based readers with family, assets, or financial interest in India, these schemes are more than just interest-bearing accounts, they are time-tested tools for securing long-term returns. As of July 2025, India’s Ministry of Finance has maintained the existing rates for popular small savings schemes, setting a consistent tone for the second quarter of the financial year.

What Are Small Savings Schemes?

Small savings schemes are government-backed deposit plans in India that offer fixed interest rates and low-risk returns. They're ideal for long-term savers, especially those looking to diversify portfolios beyond volatile equities. The interest is revised quarterly, ensuring these tools stay competitive with market trends. For Non-Resident Indians (NRIs) and U.S. residents with Indian ties, these instruments offer a stable investment channel.

Small Savings Scheme Interest Rate 2025: Key Highlights

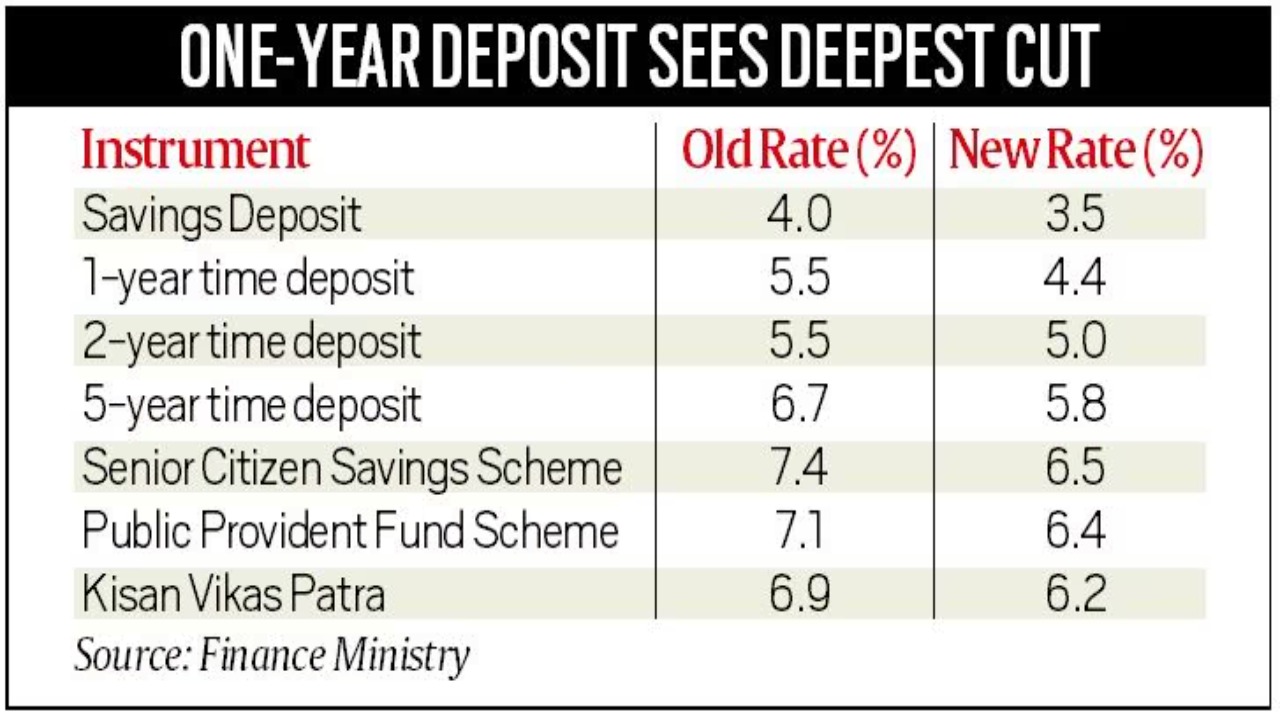

The latest update from the Department of Economic Affairs confirms that the Small savings scheme interest rate 2025 remains unchanged for the July–September quarter. Here’s a detailed breakdown:

|

Scheme Name |

Interest Rate (Jul–Sep 2025) |

|

Public Provident Fund (PPF) |

7.1% |

|

Sukanya Samriddhi Yojana (SSY) |

8.2% |

|

Senior Citizen Savings Scheme (SCSS) |

8.2% |

|

National Savings Certificate (NSC) |

7.7% |

|

Kisan Vikas Patra (KVP) |

7.5% (Matures in 115 months) |

|

Post Office Savings Account |

4.0% |

|

Post Office Monthly Income Scheme (MIS) |

7.4% |

|

Post Office 3-Year Time Deposit |

7.1% |

|

Post Office 5-Year Recurring Deposit |

6.7% |

The announcement aligns with the Small Savings Scheme interest rate Affairscloud reports, confirming a steady course by the Indian government to provide stability for savers amid global economic uncertainties.

Why the Rates Remain Unchanged: Economic Stability Over Surprises

The decision to keep the Small saving schemes interest rates unchanged for July reflects the Indian government's conservative yet calculated financial approach. While inflation and bond yields have shown fluctuations, maintaining the same rates helps build confidence among investors, especially senior citizens and middle-income families who rely on these schemes for predictable returns.

From a macroeconomic standpoint, stability in these rates helps balance liquidity in the economy without encouraging excessive consumption or high-risk speculation. It also reassures both local and global investors that the government values consistent, inflation-beating instruments.

Breaking Down the Popular Schemes

Public Provident Fund (PPF):

Offering 7.1%, this 15-year plan remains a favorite. It’s exempt-exempt-exempt (EEE) for tax purposes, meaning contributions, interest earned, and maturity amount are all tax-free.

Sukanya Samriddhi Yojana (SSY):

With 8.2%, this plan supports girl child education and marriage expenses. The high return rate makes it one of the most rewarding options currently available.

Senior Citizen Savings Scheme (SCSS):

Matching SSY at 8.2%, SCSS continues to be a top choice for retirees looking for assured income. It’s backed by a sovereign guarantee, making it extremely safe.

National Savings Certificate (NSC):

At 7.7%, NSC provides a 5-year lock-in and is eligible for tax deduction under Section 80C, ideal for conservative savers.

Post Office Time & Recurring Deposits:

Although slightly lower in return, these schemes attract small investors who prefer short-term commitments with government backing.

Smart Takeaways for U.S.-Based Investors

-

Currency Exchange Benefits:

With the rupee often trading at favorable rates against the U.S. dollar, investing in rupee-based assets like small savings schemes can yield higher real returns for U.S. residents. -

Diversification Strategy:

These schemes add a layer of fixed-income security to otherwise equity-heavy U.S. portfolios. -

Family Financial Planning:

Many U.S.-based individuals manage savings for aging parents or children in India. Understanding Small saving schemes interest rate changes ensures well-informed decisions and better planning. -

Risk-Adjusted Returns:

Even though the rates are unchanged, they beat current inflation levels in India, delivering solid real returns with virtually no credit risk.

Why It Matters in 2025

2025 is shaping up to be a year of cautious optimism. With global interest rates still balancing between control and correction, the Indian government’s decision to keep rates steady is a nod to predictability and long-term vision.

For investors comparing returns across countries, India’s small savings rates continue to offer better yield-to-risk ratios than many U.S. savings instruments. When adjusted for exchange rate movement and inflation, these instruments can still generate real income advantages.

How to Monitor These Rates Moving Forward

Staying informed is essential. Platforms like Small Savings Scheme interest rate Affairscloud provide timely updates, analysis, and predictions. For the July 2025 quarter, their projections aligned with official government decisions, underscoring their reliability.

Bookmarking trusted sources and subscribing to notifications from India’s Finance Ministry can also help U.S.-based investors stay ahead of changes.

Final Thought: Small Steps, Big Security

The consistency in the Small saving schemes interest rate is more than just a fiscal number, it’s a vote of confidence for millions of savers. Whether for a child’s education, retirement corpus, or tax-saving strategy, these instruments offer a roadmap toward financial stability. And in 2025, that stability is gold.

For U.S. residents navigating global investments, understanding these schemes isn’t just helpful, it’s essential. As India continues to grow economically, these small savings options remain grounded in purpose and performance.

Explore more about safe investments, currency hedging strategies, and global fixed-income tools to optimize your financial planning across borders. For more details on recent profit changes, see how National Savings profits have increased.

'%3e%3crect%20y='0.445312'%20width='48'%20height='48'%20rx='24'%20fill='white'%20fill-opacity='0.5'/%3e%3crect%20x='0.5'%20y='0.945312'%20width='47'%20height='47'%20rx='23.5'%20stroke='%23808080'/%3e%3cpath%20d='M34.625%2024.4453L14%2024.4453'%20stroke='%23808080'%20stroke-width='0.920053'/%3e%3cpath%20d='M23.375%2034.4453L13.375%2024.4453L23.375%2014.4453'%20stroke='%23808080'%20stroke-width='0.920053'/%3e%3c/g%3e%3cdefs%3e%3cfilter%20id='filter0_b_489_44344'%20x='-12'%20y='-11.5547'%20width='72'%20height='72'%20filterUnits='userSpaceOnUse'%20color-interpolation-filters='sRGB'%3e%3cfeFlood%20flood-opacity='0'%20result='BackgroundImageFix'/%3e%3cfeGaussianBlur%20in='BackgroundImageFix'%20stdDeviation='6'/%3e%3cfeComposite%20in2='SourceAlpha'%20operator='in'%20result='effect1_backgroundBlur_489_44344'/%3e%3cfeBlend%20mode='normal'%20in='SourceGraphic'%20in2='effect1_backgroundBlur_489_44344'%20result='shape'/%3e%3c/filter%3e%3c/defs%3e%3c/svg%3e)

'%3e%3crect%20y='0.445312'%20width='48'%20height='48'%20rx='24'%20fill='white'%20fill-opacity='0.5'/%3e%3crect%20x='0.5'%20y='0.945312'%20width='47'%20height='47'%20rx='23.5'%20stroke='%23808080'/%3e%3cpath%20d='M13.375%2024.4453L34%2024.4453'%20stroke='%23808080'%20stroke-width='0.920053'/%3e%3cpath%20d='M24.625%2014.4453L34.625%2024.4453L24.625%2034.4453'%20stroke='%23808080'%20stroke-width='0.920053'/%3e%3c/g%3e%3cdefs%3e%3cfilter%20id='filter0_b_489_44344'%20x='-12'%20y='-11.5547'%20width='72'%20height='72'%20filterUnits='userSpaceOnUse'%20color-interpolation-filters='sRGB'%3e%3cfeFlood%20flood-opacity='0'%20result='BackgroundImageFix'/%3e%3cfeGaussianBlur%20in='BackgroundImageFix'%20stdDeviation='6'/%3e%3cfeComposite%20in2='SourceAlpha'%20operator='in'%20result='effect1_backgroundBlur_489_44344'/%3e%3cfeBlend%20mode='normal'%20in='SourceGraphic'%20in2='effect1_backgroundBlur_489_44344'%20result='shape'/%3e%3c/filter%3e%3c/defs%3e%3c/svg%3e)